By Robert Murphy, Senior Managing Director

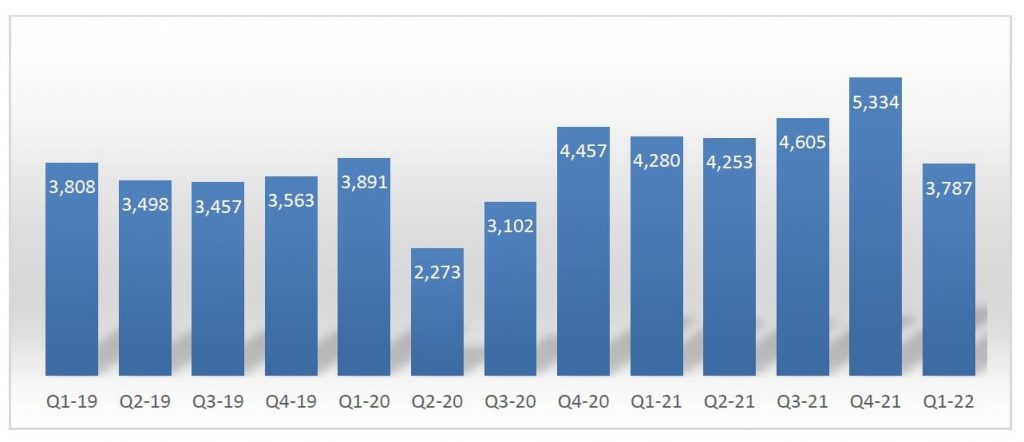

North American merger and acquisition (M&A) deal volumes slowed down in first quarter 2022 after a record-setting 2021. Year-over-year deal volume decreased 11.5% over first quarter 2021. Deal activity, nevertheless, was still in line with that of the last five years.

With strong corporate balance sheets and record private equity (PE) dry powder, companies and investors are still looking for investment opportunities despite market volatility and uncertain economic outlook. Soaring inflation, rising interest rates, the Russian-Ukraine war and ongoing supply chain disruptions are main risk factors that have recently dampened investor confidence. However, positive economic drivers, such as the progressive lifting of COVID restrictions in many countries, strong demand for labor, goods and services and low unemployment rates, will help offset some of these headwinds in M&A activity.

The pace of private equity dealmaking activity slackened from last year’s blockbuster performance. During first quarter 2022, U.S. PE firms closed 2,166 deals for a combined $330.8 billion. The U.S. Federal Reserve raised its benchmark rate from 0.25% to 0.5% in mid-March and is expected to hike up rates several times this year to counter historical high inflation.

Despite intense market volatility and interest rate pressure, significant capital still flowed into the technology sector. The appetite for deals remained strong as investors focused on attractive growth prospects amid adjusting valuations. Deal activity in technology pushed forward in first quarter, with greater deal value than in fourth quarter 2021 and is expected to remain robust.

Closed M&A Deals in North America (Q1 2019 – Q1 2022)

Source: Pitchbook & PKFIB research

While Valuations Held Steady First Quarter 2022, Risk Factors Are Looming over M&A Activity

In the first quarter of 2022, average transaction multiples with Transaction Enterprise Values (TEV) of $10 million to $250 million was 7.3x, matching the mark for all of 2021, but slightly down from the 7.5x average recorded in third and fourth quarter 2021, which was at a historical high level.

Q1 21 | Q2 21 | Q3 21 | Q4 21 | Q1 22 | |

TEV/EBITDA | 7.0x | 7.1x | 7.5x | 7.5x | 7.3x |

Total Debt/EBITDA | 4.0x | 3.6x | 4.0x | 4.2x | 3.9x |

Senior Debt/EBITDA | 3.7x | 2.8x | 3.1x | 3.3x | 3.2x |

Source: GF Data®

Higher performers with above-average trailing 12-month (TTM) EBITDA margins and sales growth continued to be rewarded with premium valuation multiples. These businesses with above average financial performance, based on TTM EBITDA margin and revenue growth, comprised 67% of total deal volume in first quarter 2022, consistent with 2021. Buyout targets with above-average financial performance were valued at an average of 7.7x, down slightly from 7.9x in 2021, but in line with the multiple average in 2020.

Quality Premium – Buyout Only

| 2013 – 2017 | 2018 | 2019 | 2020 | 2021 | YTD 2022 | Total |

Above Average Financials | 6.6x | 7.8x | 7.5x | 7.7x | 7.9x | 7.7x | 7.0x |

Other Buyouts | 6.0x | 6.4x | 6.3x | 6.1x | 6.1x | 6.3x | 6.1x |

Premium/(Discount) | 109% | 123% | 120% | 127% | 130% | 122% | 115% |

Source: GF Data®

Debt/EBITDA – All Industries by Deal Size ($10m – $250m)

| 2013 – 2017 | 2018 | 2019 | 2020 | 2021 | YTD 2022 | Total |

Total Debt/EBITDA | 3.6x | 3.8x | 3.9x | 3.7x | 4.0x | 3.9x | 3.7x |

Senior Debt/EBITDA | 2.6x | 2.9x | 3.2x | 3.1x | 3.3x | 3.2x | 2.8x |

Source: GF Data®

Debt leverage returned to the 2019 level and was in line with 2021. Total debt in first quarter Q1 2022 was 3.9x EBITDA, compared with 4.0x in 2021, 3.7x in 2020, and 3.9x in 2019, respectively.

Outlook

Looking ahead to the remaining quarters of 2022, M&A dealmaking is unlikely to achieve the same volume levels reached in 2021 but should remain at active, healthy levels. The Fed plans for six more interest rate hikes after its first one in March to fight against the highest inflation rate since 1981. Higher interest rates would lead to higher discount rate, lowering deal valuations, increasing borrowing costs and eventually building pressure on M&A activity. In the meantime, the Russia-Ukraine war will continue to weigh on global economies, resulting in elevated commodities prices and disrupted supply chains.

However, unprecedented dry powder, record high cash on corporate balance sheets and an intense demand for technology disruption and innovation across all sectors will help to keep the M&A activity strong. Events over the past two years have demonstrated the resilience of investors to global shocks.

Financial buyers will continue to weigh supply chain issues and how the business would perform in a recession in evaluating investment opportunities. Overall, we remain optimistic on M&A activity for the rest of 2022.

Contact Us

Robert Murphy

Senior Managing Director

rmurphy@pkfod.com

561.337.5324 | 201.788.6844